Reclaiming Your Time

The Desire for Choice

The traditional notion of retirement as a fixed milestone at 65 or 68 is rapidly evolving. Today’s forward-thinking individuals and families across Ireland are shifting their perspective from viewing retirement as an age-based event to understanding it as a financial status. The core goal isn’t simply reaching a certain birthday; it’s achieving enough passive income to cover your expenses, making work optional rather than mandatory.

This fundamental shift in thinking opens up possibilities that previous generations couldn’t imagine. Instead of counting down the decades until you can finally pursue your passions, you can design a life where financial security provides the freedom to choose how you spend your time.

Financial Independence vs. Retire Early

Financial Independence (FI) provides the ultimate freedom: the ability to choose whether you work because you want to, not because you have to. Retire Early (RE) represents the choice to step away from the conventional workforce once that independence is achieved. Some pursue both simultaneously, while others focus initially on FI, keeping their options open.

This article provides a strategic roadmap specifically adapted for the Republic of Ireland, acknowledging our unique tax landscape, pension regulations, and economic environment. The path to financial freedom requires careful navigation of Irish financial structures, but the destination remains the same: true choice in how you spend your most valuable resource, your time.

Calculating Your Freedom Threshold

Determining Annual Expenses

The foundation of any FIRE strategy begins with understanding exactly how much money you need to live. This requires rigorous, realistic tracking of your current annual outgoings over at least 12 months. Don’t rely on estimates or rough calculations; use bank statements, credit card bills, and receipts to build an accurate picture.

Consider how your expenses might change in early retirement. You’ll likely eliminate commuting costs, work clothing expenses, and perhaps expensive lunches. However, you might increase spending on travel, hobbies, or health insurance if you’re no longer covered by an employer scheme. Factor in potential changes like moving to a smaller property or relocating to a lower-cost area.

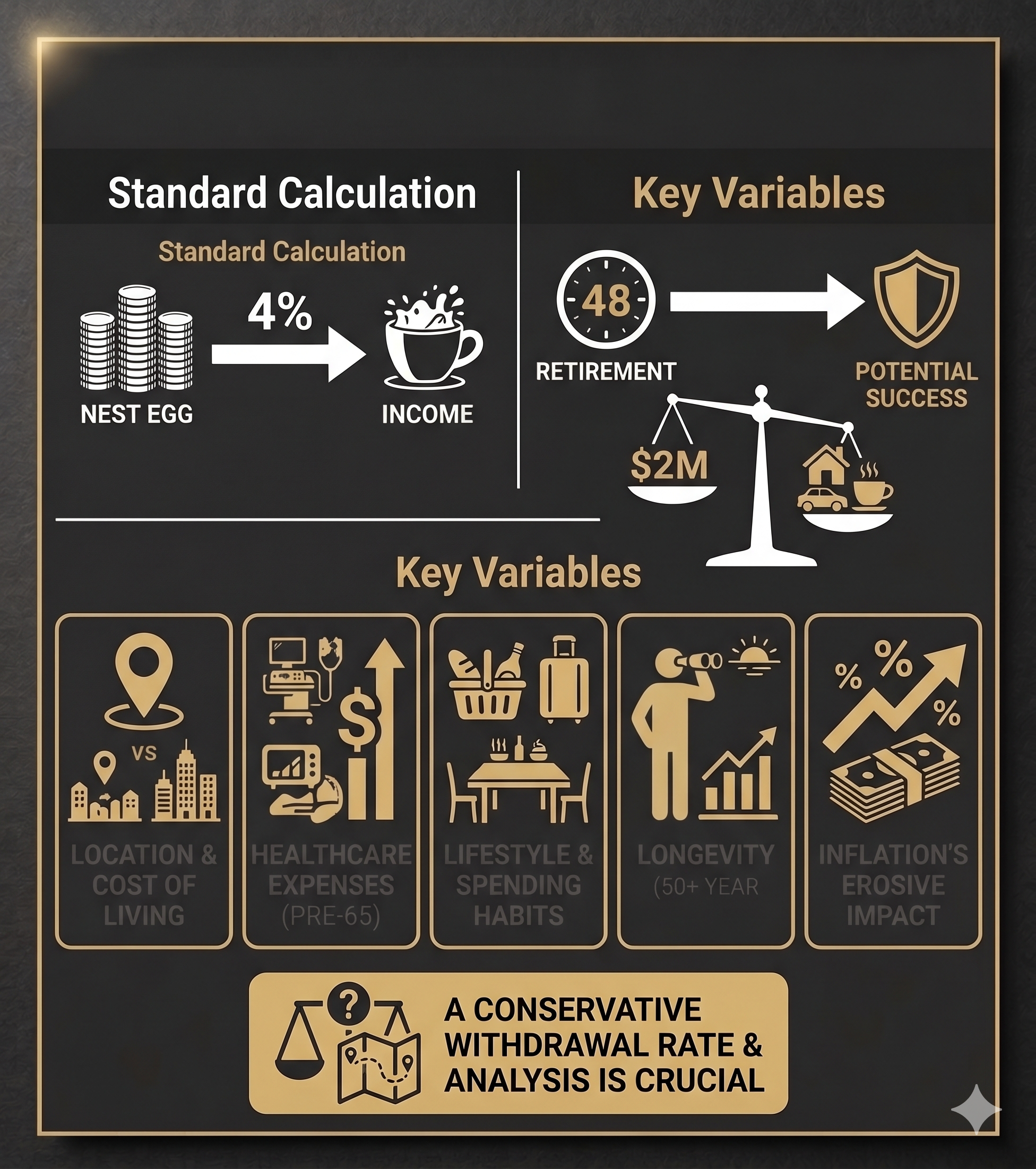

The Core Principle: The 4% Rule

The cornerstone of FIRE planning is the 4% rule, which emerged from historical analysis of portfolio performance over rolling 30-year periods. The principle suggests you can safely withdraw 4% of your investment portfolio annually, adjusted for inflation, without depleting your capital over a typical retirement period.

Your FIRE Number = Annual Expenses × 25

If you need £40,000 annually to maintain your lifestyle, your FIRE number would be £1,000,000. This calculation assumes your investment portfolio can sustainably support a 4% annual withdrawal rate. The mathematical foundation underlying this approach stems from decades of research into sustainable withdrawal strategies and market performance, which demonstrates how properly diversified portfolios can support long-term financial independence.

Understanding the Variations

Lean FIRE targets the minimum viable retirement lifestyle, often requiring significant lifestyle adjustments and frugal living. This approach might suit those comfortable with modest accommodation, minimal discretionary spending, and careful budgeting.

Fat FIRE maintains a comfortable, higher-spending retirement lifestyle without significant compromises. This typically requires FIRE numbers of £2 million or more, depending on your desired standard of living.

Barista FIRE has particular appeal in the Irish context due to our progressive tax system. This approach involves retiring early whilst maintaining part-time or low-stress work for supplementary income. Lower earnings often result in substantially lower tax rates, making this strategy especially attractive for those who enjoy some structure or social interaction through work.

Phase 1: Maximising the Accumulation Rate

The Power of the Savings Rate

Your savings rate (the percentage of income you save and invest) has more impact on reaching FIRE than investment returns, particularly in the early stages. A person earning £50,000 who saves 50% will accumulate wealth faster than someone earning £100,000 who saves 10%, despite the higher earner having double the income.

Aggressive savings targets of 40-60% or more dramatically accelerate your journey to financial independence. Each pound saved serves a dual purpose: it reduces the annual expenses you need to cover in retirement whilst simultaneously building the investment portfolio that will generate your passive income.

Controlling Lifestyle Creep

Lifestyle creep (the gradual increase in spending as income rises) is the silent killer of FIRE aspirations. Combat this through conscious spending and robust budgeting systems. Many successful FIRE practitioners use the 50/30/20 rule as a starting point: 50% for needs, 30% for wants, and 20% for savings, then aggressively optimise from there.

Distinguish clearly between genuine needs, mere wants, and expenses that align with your core values. A £5 daily coffee might seem insignificant, but £1,825 annually could reduce your FIRE timeline by months when invested consistently. Focus on high-impact changes: housing, transport, and food typically represent the largest opportunities for optimisation.

Generating Additional Income

Increasing your income accelerates wealth accumulation more effectively than extreme frugality alone. Negotiate salary increases, pursue promotions, or consider career changes to higher-paying fields. Document your achievements, research market rates, and present compelling cases for advancement.

Explore entrepreneurial opportunities or side businesses that leverage your existing skills. Freelance consulting, online businesses, or service-based ventures can generate substantial additional income without requiring significant upfront capital. The key is treating extra income as acceleration fuel for your FIRE journey, not lifestyle enhancement.

Phase 2: Tax-Efficient Investing (The Irish Angle)

Leveraging Pension Advantages

Irish pension contributions offer unparalleled tax advantages, especially for higher-rate taxpayers. Contributions receive immediate tax relief at your marginal rate, meaning a £1,000 contribution only costs a 40% taxpayer £600 after tax relief. This represents an instant 67% return on investment before any market growth.

Maximise Additional Voluntary Contributions (AVCs) up to the age-based limits: 15% of income under age 30, increasing by 5% every decade to 40% for those aged 60-69. Understand the distinction between occupational pension schemes and Personal Retirement Savings Accounts (PRSAs) as both offer tax advantages, but with different features and flexibility.

Navigating the Investment Landscape

Index funds and ETFs form the backbone of most successful FIRE portfolios due to their low costs, broad diversification, and consistent long-term performance. Global equity trackers provide exposure to thousands of companies across multiple countries and sectors, reducing concentration risk whilst capturing overall market growth.

However, Irish investors face the significant challenge of deemed disposal and exit tax on non-domiciled ETFs. This complex regulation requires paying 41% tax on gains every eight years, even without selling. Understanding these rules and exploring strategies to mitigate their impact (such as using Irish-domiciled funds or specific investment structures) is crucial for optimising after-tax returns.

Considering Other Tax-Efficient Vehicles

Pension wrappers provide completely tax-free growth until withdrawal, making them extremely powerful wealth-building vehicles despite access restrictions. For the gap years between early retirement and pension access, taxable investments become necessary.

Consider using Non-Approved Retirement Funds (NARFs) or other bridge strategies for covering expenses during the pre-pension access period. Balance the tax efficiency of pensions against the flexibility of accessible investments based on your specific timeline and goals.

Phase 3: The Transition and Withdrawal Strategy

Bridging the Gap

Planning for the years between early retirement and pension access requires careful strategy. Occupational pensions typically allow access from age 50, whilst PRSAs and ARFs become available at 55. This gap period requires funding from taxable savings, rental income, or specifically designed bridge investments.

Calculate precisely how much you’ll need during this bridge period and ensure these funds are held in accessible accounts. Consider the tax implications of different withdrawal strategies and time your exit from employment to optimise your overall tax position.

Managing Longevity and Inflation Risk

The 4% rule provides a solid foundation, but real life requires flexibility and ongoing monitoring. Advanced practitioners use Monte Carlo simulations to stress-test their withdrawal strategies against various market scenarios and economic conditions. These models help identify the probability of portfolio success over different time horizons and market conditions.

Build inflation hedges into your portfolio through assets that historically maintain purchasing power over time. Real Estate Investment Trusts (REITs), inflation-linked bonds, and equity holdings in companies with pricing power can help protect against the erosive effects of rising prices over multi-decade retirement periods.

State Pension and PRSI Considerations

Don’t overlook your entitlement to the State Pension (Contributory), which provides valuable income security in later life. Maintaining sufficient PRSI contributions remains important even after leaving full-time employment. Consider making voluntary contributions if your early retirement might otherwise create gaps in your contribution record.

The State Pension currently requires 520 qualifying contributions for a reduced pension or 2,080 contributions for the full rate. Factor this future income stream into your overall retirement planning, as it can significantly reduce the private wealth required for complete financial independence.

Enjoying the Financial Latitude

Focus on Purpose

Financial independence without purpose can lead to unexpected challenges. Research consistently shows that successful early retirees have clear plans for how they’ll spend their newfound freedom. Whether through volunteering, creative pursuits, travel, family time, or passion projects, identify meaningful activities that will provide structure and fulfilment beyond the traditional 9-to-5.

Consider gradually reducing your work commitments rather than stopping abruptly. Many find that consulting, part-time roles, or project-based work provides an ideal transition whilst maintaining some routine and social interaction.

Continuous Review

Financial independence is an ongoing state requiring regular monitoring, not a destination you reach once and forget. Conduct annual reviews of your expenses, portfolio performance, withdrawal rates, and goals. Market conditions, personal circumstances, and economic factors will inevitably change over time.

Build flexibility into your plans. Be prepared to adjust your withdrawal rate during market downturns, increase spending during strong performance periods, or modify your lifestyle based on changing priorities or health considerations.

Final Thoughts

This blueprint provides the structural framework for achieving financial independence, but the real prize is the freedom it delivers: freedom to choose how you spend your time, energy, and attention. The path requires discipline, planning, and patience, but thousands of individuals and families have successfully walked this road before you.

The journey begins with a single step: understanding exactly where you stand today and where you want to go tomorrow. Start tracking your expenses, maximise your savings rate, and invest those savings in a diversified, low-cost portfolio whilst taking full advantage of Ireland’s pension tax benefits.

Your future self will thank you for the courage to begin today.